By LINLEY SANDERS and AMELIA THOMSON-DEVEAUX, Associated Press

WASHINGTON (AP) — President Donald Trump got a significant amount of blame during the last partial government shutdown, which took place toward the end of his first term after he forced a shutdown over border wall funding — but with Democrats embracing the shutdown fight this time, the outcome could be very different.

A New York Times/Siena poll conducted last week, prior to the shutdown, shows that most registered voters did not want Democrats to shut down the government if their demands were not met, although both parties could end up receiving some blame for the resulting closure.

Here is what AP-NORC polling showed about the 2019 shutdown, and what recent polling suggests about how voters could react as the current shutdown unfolds.

Many blamed Trump for the last partial government shutdown

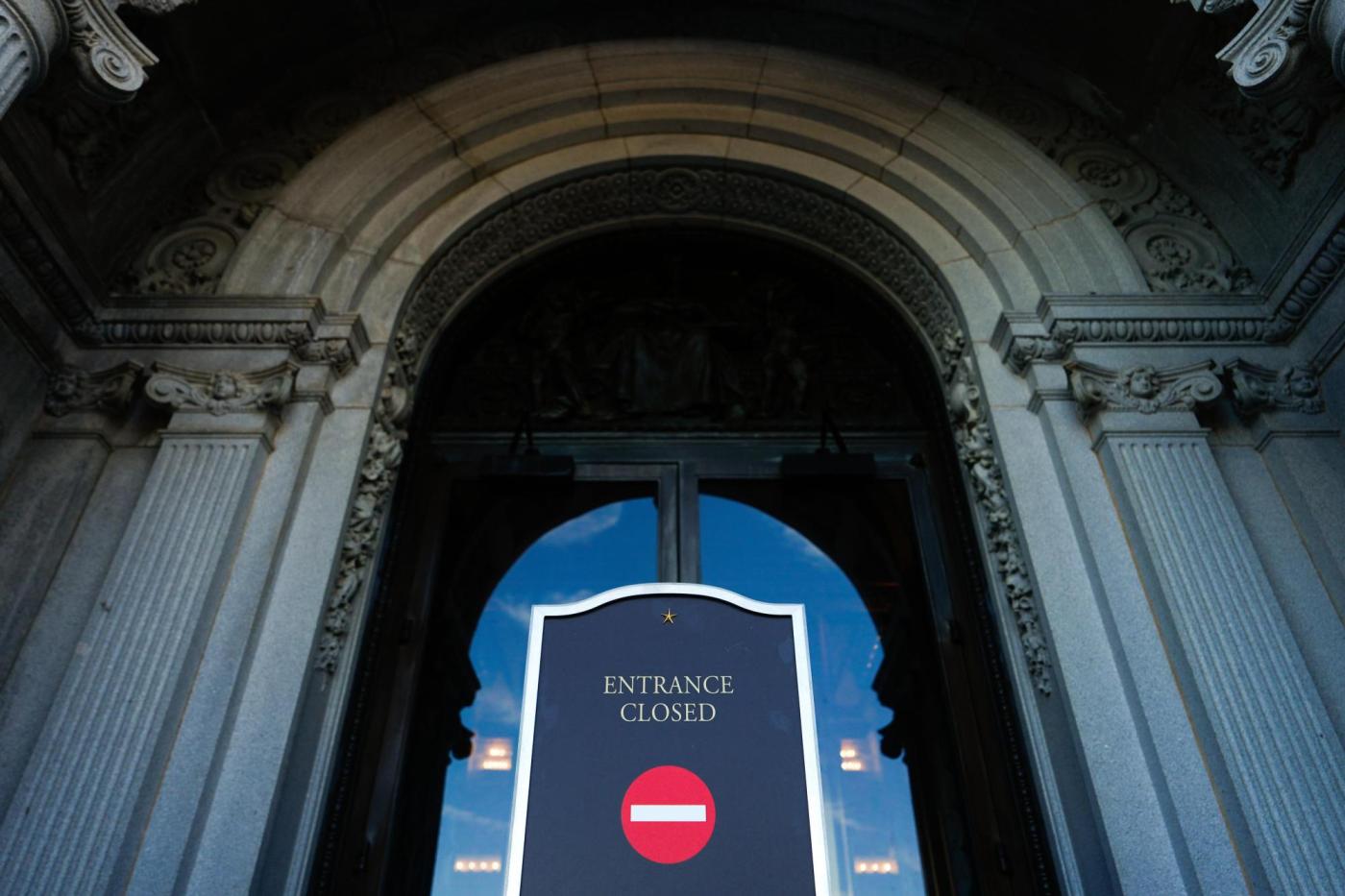

The last government shutdown took place in late 2018 and early 2019, after Trump demanded money for a U.S.-Mexico border wall. Then-House Speaker Nancy Pelosi, a Democrat, refused to negotiate unless Trump allowed the government to reopen.

In an AP-NORC poll conducted during that shutdown, about 7 in 10 Americans said Donald Trump had “a great deal” or “quite a bit” of responsibility for the partial shutdown. About 6 in 10 said that about Republicans in Congress, and roughly half said that about Democrats in Congress.

It was seen as a significant problem at the time, as airport delays and missed paychecks for federal workers brought urgency to efforts to resolve the standoff. About two-thirds of U.S. adults said the partial government shutdown was “a major problem for the country.” Democrats were more likely than Republicans to see it as a large issue.

Most didn’t want Democrats to force a shutdown this time

In the Times/Siena poll, about two-thirds of registered voters said the Democrats should not shut down the government, even if their demands were not met.

Democrats in Congress had demanded an extension to expiring health care benefits in order to pass the bill to extend government funding. Republicans in Congress had refused, but offered a stopgap bill to keep the government open for several weeks, which Democrats rejected.

Related Articles

New York rapper who joined Trump at campaign rally sentenced to 5 years for attempted murder

As Trump punts on medical debt, battle over patient protections moves to states

The US military has long been an engine of social change. Hegseth’s approach runs counter to that

States target ultraprocessed foods in bipartisan push

Cuban foreign minister says Rubio’s ‘personal’ agenda in Latin America risks Trump’s peace prospects

Registered Democrats may have been more eager than voters overall to see their party’s leadership force a shutdown: 47% said the Democrats should refuse to fund the government if their demands were not met. The move was less popular among independents and Republicans. About 9 in 10 Republicans and roughly 6 in 10 independents said Democrats should not shut down the government, even if their demands were not met.

But depending on what happens next, there could be plenty of blame to go around.

About one-quarter of registered voters in the Times/Siena poll — which was conducted prior to the shutdown — said they would blame Trump and the Republicans in Congress if a shutdown happened, while about 2 in 10 said they would place blame on congressional Democrats. About one-third said they’d blame both sides equally.

What Americans think of Congress

Congress had few fans with the American public, even before the shutdown.

It’s hard to find an American who has “a great deal” of confidence in the way Congress is being run, according to AP-NORC polling. Only 6% said they had a high level of confidence in the people running Congress in polling from this summer. About half had “only some” and 44% had hardly any confidence in how Congress was being run.

Confidence tends to be low among Democrats and Republicans, regardless of which party is in power. About 1 in 10 Republicans had “a great deal” of confidence in Congress, compared to 2% of Democrats.

St. Paul’s Highland District Council and other community groups are hosting a forum on Monday where voters can ask candidates running for mayor questions.

The forum is hosted by the district council, FairVote Minnesota, Danger Boat Productions, and others.

It will take place from 6:30 to 8:30 p.m. at Gloria Dei Lutheran Church in St. Paul. Those interested can RSVP and send in questions at the Fair Vote MN website or Rank Your Vote website.

The first part will be a question and answer period.

The forum will feature Mayor Melvin Carter, Yan Chen, Adam Dullinger, State Rep. Kaohly Her and Mike Hilborn. Carter is running for his third term as mayor.

After the forum, residents can meet face to face with the candidates.

Related Articles

St. Paul mayoral candidates debate rising property taxes, loss of Cub Foods

League of Women Voters sponsors St. Paul mayoral forum Wednesday

Letters: A madness in the land

St. Paul mayor’s race begins in earnest, Kaohly Her launches campaign

Owamni, the award-winning native restaurant from chef Sean Sherman, will relocate just down the river to the restaurant space on the main floor of the Guthrie Theater in the spring of 2026.

The restaurant, part of the nonprofit group North American Traditional Indigenous Food Systems, will double in size by moving out of its original spot in the Water Works Pavilion.

“We are so grateful to the Minneapolis Park and Recreation Board and Water Works Pavilion for giving Owamni our solid start — we outgrew our original location almost from the moment we opened,” Sherman said in a news release. “The Guthrie space gives us the opportunity to share Indigenous cuisine with more diners, and we can’t wait to bring it to life.”

Owamni opened in 2021 to immediate acclaim, and with that came difficulty scoring a reservation. The restaurant focuses on ingredients native to our land, avoiding commodities introduced by colonizers such as wheat flour, dairy and sugar. The James Beard Foundation named it the Best New Restaurant in 2022, cementing its importance — and popularity.

The original location was chosen for its proximity to the river, something that will remain with its new spot, which has housed many excellent restaurants over the years. The last restaurant to occupy the space, Sea Change, shut down during the pandemic and never reopened.

“Owamni means ‘falling water’ in the Dakota language, and we’re so glad to remain close to St. Anthony Falls, on the shores of the Mississippi, which is a source of great significance to the Dakota people,” Sherman said.

Related Articles

Osteria I Nonni in Lilydale to close this month; Buon Giorno Deli hoping to relocate

Girl Scouts drop Exploremores: Is the new ‘rocky road’ cookie worth the hype?

Marinated pork tenderloin stars in this budget weeknight meal

With a skillet, moussaka doesn’t have to be a project dish

Jane Goodall, the conservationist renowned for her groundbreaking chimpanzee field research and globe-spanning environmental advocacy, has died. She was 91.

The Jane Goodall Institute announced the primatologist’s death Wednesday in an Instagram post. According to the institute, Goodall died of natural causes while in California on a U.S. speaking tour.

Her discoveries “revolutionized science, and she was a tireless advocate for the protection and restoration of our natural world,” the Institute said.

While living among chimpanzees in Africa decades ago, Goodall documented the animals using tools and doing other activities previously believed to be exclusive to humans, and also noted their distinct personalities. Her observations and subsequent magazine and documentary appearances in the 1960s transformed how the world perceived not only humans’ closest living biological relatives but also the emotional and social complexity of all animals, while propelling her into the public consciousness.

“Out there in nature by myself, when you’re alone, you can become part of nature and your humanity doesn’t get in the way,” she told The Associated Press in 2021. “It’s almost like an out-of-body experience when suddenly you hear different sounds and you smell different smells and you’re actually part of this amazing tapestry of life.”

Jane Goodall poses for a portrait with her stuffed monkey Mr. H. After speaking to students and adults during her “Roots & Shoots” program at the Oakland Zoo in Oakland, Calif., on Thursday, Oct. 6, 2022. Goodall, 88, is the world’s leading expert on chimpanzees. (Jane Tyska/Bay Area News Group)

President Joe Biden, right, presents the Presidential Medal of Freedom, the Nation’s highest civilian honor, to conservationist Jane Goodall in the East Room of the White House, Jan. 4, 2025, in Washington. (AP Photo/Manuel Balce Ceneta, File)

English primatologist and anthropologist Jane Goodall speaks on a panel “Earth’s Wisdom Keepers” at the forum’s annual meeting in Davos, Switzerland, Jan. 19, 2024. (AP Photo/Markus Schreiber, File)

Primatologist Jane Goodall goes through slides before making a presentation in Chicago, May 9, 1982. (AP Photo/Charles Knoblock, file)

Jane Goodall kisses Tess, a female chimpanzee, at the Sweetwaters Chimpanzee Sanctuary near Nanyuki, north of Nairobi, on Dec. 6, 1997. (AP Photo/Jean-Marc Bouju, File)

Dr. Jane Goodall smiles before speaking at the University of Montana President’s Lecture Series in Missoula, Mont., June 26, 2022. (AP Photo/Tommy Martino, File)

French Foreign Minister Laurent Fabius, from left, primatologist Jane Goodall, former U.S. Vice President Al Gore, New York Mayor Bill de Blasio and U.N. Secretary General Ban Ki-moon participate in the People’s Climate March in New York, Sept. 21, 2014. (AP Photo/Craig Ruttle, File)

Primatologist Jane Goodall kisses Pola, a 14-months-old chimpanzee baby from the Budapest Zoo, that she symbolically adopted in Budapest, Hungary, on Dec. 20, 2004. (AP Photo/Bela Szandelszky, File)

Jane Goodall plays with Bahati, a 3-year-old female chimpanzee, at the Sweetwaters Chimpanzee Sanctuary near Nanyuki, north of Nairobi, on Dec. 6, 1997. (AP Photo/Jean-Marc Bouju, File)

1 of 9

Jane Goodall poses for a portrait with her stuffed monkey Mr. H. After speaking to students and adults during her “Roots & Shoots” program at the Oakland Zoo in Oakland, Calif., on Thursday, Oct. 6, 2022. Goodall, 88, is the world’s leading expert on chimpanzees. (Jane Tyska/Bay Area News Group)

In her later years, Goodall devoted decades to education and advocacy on humanitarian causes and protecting the natural world. In her usual soft-spoken British accent, she was known for balancing the grim realities of the climate crisis with a sincere message of hope for the future.

From her base in the British coastal town of Bournemouth, she traveled nearly 300 days a year, even after she turned 90, to speak to packed auditoriums around the world. Between more serious messages, her speeches often featured her whooping like a chimpanzee or lamenting that Tarzan chose the wrong Jane.

While first studying chimps in Tanzania in the early 1960s, Goodall was known for her unconventional approach. She didn’t simply observe them from afar but immersed herself in every aspect of their lives. She fed them and gave them names instead of numbers, something for which she received pushback from some scientists.

Her findings were circulated to millions when she first appeared on the cover of National Geographic in 1963 and soon after in a popular documentary. A collection of photos of Goodall in the field helped her and even some of the chimps become famous. One iconic image showed her crouching across from the infant chimpanzee named Flint. Each has arms outstretched, reaching for the other.

In 1972, the Sunday Times published an obituary for Flo, Flint’s mother and the dominant matriarch, after she was found face down on the edge of a stream. Flint died about three weeks later after showing signs of grief, eating little and losing weight.

″What the chimps have taught me over the years is they’re so like us. They’ve blurred the line between humans and animals,″ she told The Associated Press in 1997.

Goodall has earned top civilian honors from a number of countries including Britain, France, Japan and Tanzania. She was awarded the Presidential Medal of Freedom in 2025 by then-U.S. President Joe Biden and won the prestigious Templeton Prize in 2021.

“Her groundbreaking discoveries have changed humanity’s understanding of its role in an interconnected world, and her advocacy has pointed to a greater purpose for our species in caring for life on this planet,” said the citation for the Templeton Prize, which honors individuals whose life’s work embodies a fusion of science and spirituality.

Goodall was also named a United Nations Messenger of Peace and published numerous books, including the bestselling autobiography “Reason for Hope.”

Born in London in 1934, Goodall said her fascination with animals began around when she learned to crawl. In her book, “In the Shadow of Man,” she described an early memory of hiding in a henhouse to see a chicken lay an egg. She was in there so long her mother reported her missing to the police.

Related Articles

How ‘woke’ went from an expression in Black culture to a conservative criticism

The US military has long been an engine of social change. Hegseth’s approach runs counter to that

States target ultraprocessed foods in bipartisan push

AOL’s dial up internet takes its last bow, marking the end of an era

Former judge is likely the next leader of the Mormon church and its 17 million members

She bought her first book — Edgar Rice Burroughs’ “Tarzan of the Apes” — when she was 10 and soon made up her mind about her future: Live with wild animals in Africa.

That plan stayed with her through a secretarial course when she was 18 and two different jobs. And by 1957, she accepted an invitation to travel to a farm in Kenya owned by a friend’s parents.

It was there that she met the famed anthropologist and paleontologist Louis Leakey at a natural history museum in Nairobi, and he gave her a job as an assistant secretary.

Three years later, despite Goodall not having a college degree, Leakey asked if she would be interested in studying chimpanzees in what is now Tanzania. She told the AP in 1997 that he chose her “because he wanted an open mind.”

The beginning was filled with complications. British authorities insisted she have a companion, so she brought her mother at first. The chimps fled if she got within 500 yards (460 meters) of them. She also spent weeks sick from what she believes was malaria, without any drugs to combat it.

But she was eventually able to gain the animals’ trust. By the fall of 1960 she observed the chimpanzee named David Greybeard make a tool from twigs and use it to fish termites from a nest. It was previously believed that only humans made and used tools.

She also found that chimps have individual personalities and share humans’ emotions of pleasure, joy, sadness and fear. She documented bonds between mothers and infants, sibling rivalry and male dominance. In other words, she found that there was no sharp line between humans and the animal kingdom.

In later years, she discovered chimpanzees engage in a type of warfare, and in 1987 she and her staff observed a chimp “adopt” a 3-year-old orphan that wasn’t closely related.

Goodall received dozens of grants from the National Geographic Society during her field research tenure, starting in 1961.

In 1966, she earned a Ph.D. in ethology — becoming one of the few people admitted to University of Cambridge as a Ph.D. candidate without a college degree.

Her work moved into more global advocacy after she watched a disturbing film of experiments on laboratory animals at a conference in 1986.

″I knew I had to do something,″ she told the AP in 1997. ″It was payback time.″

When the COVID-19 pandemic hit in 2020 and halted her in-person events, she began podcasting from her childhood home in England. Through dozens of “Jane Goodall Hopecast” episodes, she broadcast her discussions with guests including U.S. Sen. Cory Booker, author Margaret Atwood and marine biologist Ayana Elizabeth Johnson.

“If one wants to reach people; If one wants to change attitudes, you have to reach the heart,” she said during her first episode. “You can reach the heart by telling stories, not by arguing with people’s intellects.”

In later years, she pushed back on more aggressive tactics by climate activists, saying they could backfire, and criticized “gloom and doom” messaging for causing young people to lose hope.

In the lead-up to 2024 elections, she co-founded “Vote for Nature,” an initiative encouraging people to pick candidates committed to protecting the natural world.

She also built a strong social media presence, posting to millions of followers about the need to end factory farming or offering tips on avoiding being paralyzed by the climate crisis.

Her advice: “Focus on the present and make choices today whose impact will build over time.”

The Associated Press’ climate and environmental coverage receives financial support from multiple private foundations. AP is solely responsible for all content. Find AP’s standards for working with philanthropies, a list of supporters and funded coverage areas at AP.org.

Related Articles

Obituary: Veteran TV and radio broadcaster Stan Turner was ‘one of the great storytellers’

Sonny Curtis, Crickets member who penned ‘Mary Tyler Moore Show’ theme, dies at 88

Robert Redford’s neighbors reveal his quiet, ‘sad’ life in California

Marilyn Hagerty, Grand Forks Herald columnist whose Olive Garden review went viral, dies at 99

Polly Holliday, theater star famous as the tart waitress Flo on sitcom ‘Alice,’ dies at 88